No estas registrado.

#121 04-12-15 09:55

- Tatan_79

- Miembro

- Calificacion : 62

Re: BONOS GILDEMEISTER

Tatan....no digas estupideces...tengo los bonos en mi poder....por favor infórmate cuando "aportes" al foro...no hables de lo que tu crees.... habla de lo que te consta...

Porfiado

USA-CAL

Se va a restructurar si o si esa deuda.

a los antiguos bonistas, les entregaran nuevos bonos, a plazo a mayor con una "quita" + acciones valoradas en "X"

Los antiguos bonos ya no existiran.

El Lobo de Sanhattan !!

Desconectado

#122 04-12-15 10:06

- Rolex

- Miembro

Re: BONOS GILDEMEISTER

Tatan_79 ...para que te desgastas?

USA-CAL cuando alguien le refuta algo, se molesta, cosa de ver lo que dijo sobre el tema de repatriacion de capitales. Mejor evitar confrontacion y dejar que las cosas ocurran.

Real estate cannot be lost or stolen, nor can it be carried away. Purchased with common sense, paid for in full, and managed with reasonable care, it is about the safest investment in the world

Desconectado

#123 04-12-15 11:29

- Tatan_79

- Miembro

- Calificacion : 62

Re: BONOS GILDEMEISTER

tranqui , tranqui

paz y amor.

El Lobo de Sanhattan !!

Desconectado

#124 04-12-15 14:34

- Walhalla

- Miembro

- Calificacion : 1

Re: BONOS GILDEMEISTER

Hay canje con quita, pero la quita son acciones recomprar les a valor par en 10 años. Además hay garantías que cubre app 50% del valor de deuda total por lo que sería la máxima perdida 50%. Está bien estructurado (para el emisor) y los vultures fund que Compraron s menos de un 50%. Los flujos de la empresa pueden ser cualquier cosa y que está indexado a dólar al 2021 o 2022 ... Y el que diga que lo puede predecir (dólar de 7 años más)... Es un carrilero... Si estuviera con caja para esperar 3 años ... Feliz compro bajo el 60% ... Que coincide con la quit respaldada por acciones. Si quiebra, los activos ajustados cubren un 50% de la deuda

Desconectado

#125 04-12-15 14:50

- Tatan_79

- Miembro

- Calificacion : 62

Re: BONOS GILDEMEISTER

Hay canje con quita, pero la quita son acciones recomprar les a valor par en 10 años. Además hay garantías que cubre app 50% del valor de deuda total por lo que sería la máxima perdida 50%. Está bien estructurado (para el emisor) y los vultures fund que Compraron s menos de un 50%. Los flujos de la empresa pueden ser cualquier cosa y que está indexado a dólar al 2021 o 2022 ... Y el que diga que lo puede predecir (dólar de 7 años más)... Es un carrilero... Si estuviera con caja para esperar 3 años ... Feliz compro bajo el 60% ... Que coincide con la quit respaldada por acciones. Si quiebra, los activos ajustados cubren un 50% de la deuda

Si, por lo general las "quitas" te las recompensan con acciones, valoradas en "X" (monto siempre inflado)

Lo que hay que tener claro es que siempre en una reestructuracion de deuda, el acreedor (tenedor de bonos) saldra peor parado de como entro.

de eso se trata la reestructuracion, quitarle US$ al acreedor en favor de la empresa en problemas.

Y por lo general existen mas de una reestructuracion o "quita", en un proceso como este, esta no sera la unica.

El Lobo de Sanhattan !!

Desconectado

#126 04-12-15 14:53

- Walhalla

- Miembro

- Calificacion : 1

Re: BONOS GILDEMEISTER

Así es, lo que ocurre es que la Tir es menor que el valor de recuperación vía liquidación de activos. Dado esto, es que parece un negocio bueno...

Desconectado

#127 04-12-15 15:02

- Tatan_79

- Miembro

- Calificacion : 62

Re: BONOS GILDEMEISTER

Así es, lo que ocurre es que la Tir es menor que el valor de recuperación vía liquidación de activos. Dado esto, es que parece un negocio bueno...

valor liquidacion de activos, es un valor muy, pero muy "teorico"

en la mayoria de estos casos nunca se llega a una "liquidacion de activos"

Lo mas probable es que existan nuevas restructuraciones y "quitas"

El Lobo de Sanhattan !!

Desconectado

#128 09-12-15 10:09

- ALEX TIGER

- Miembro

- Calificacion : 77

Re: BONOS GILDEMEISTER

Que interesante.

Bueno, pero nadie repara del nefasto management de AG. De aqui al '21 es opción puedan perder la licencia de HY (>85% Ventas)? Todas las demás divisiones son marginales (Especialmente FLTZ que no prendió). Atte

(2x2=5-1) Todo podrìa suceder de manera distinta a como creemos

Desconectado

#129 09-12-15 10:58

- Rolex

- Miembro

Re: BONOS GILDEMEISTER

Perder Hyundai? Primera vez que escucho eso, no pense que podia ser opcion.

Real estate cannot be lost or stolen, nor can it be carried away. Purchased with common sense, paid for in full, and managed with reasonable care, it is about the safest investment in the world

Desconectado

#130 09-12-15 11:04

- DanielAhora

- Expulsado

- Calificacion : 0

Re: BONOS GILDEMEISTER

Gildemeister es una empresa que está quebrada, solo falta que un acreedor solicite la quiebra, esto ocurrirá en cualquier momento.

Desconectado

#131 09-12-15 11:07

- Tatan_79

- Miembro

- Calificacion : 62

Re: BONOS GILDEMEISTER

Ahora si nos estamos entendiendo, precio bono = 37,7% valor par

http://www.boerse-berlin.com/index.php/ … P06006AA10

Ese podria ser un valor mas acorde para un bono en default o en riesgos de default.

NO 50%-60% valor par

El Lobo de Sanhattan !!

Desconectado

#132 10-12-15 15:02

- cristianc

- Miembro

- Calificacion : 7

Re: BONOS GILDEMEISTER

Desconectado

#133 10-12-15 15:11

- Rolex

- Miembro

Re: BONOS GILDEMEISTER

Pero si USA-CAL dijo que pusieron de rodillas al controlador, asi como smsaam vale mas que codelco, o luksic compro vapores porque todos sus hijos sobrinos y demases son unos "pelotudos" ...en fin, una vez mas le juega en contra la realidad.

Y pensar que da consejos.

Real estate cannot be lost or stolen, nor can it be carried away. Purchased with common sense, paid for in full, and managed with reasonable care, it is about the safest investment in the world

Desconectado

#134 10-12-15 15:19

- Tatan_79

- Miembro

- Calificacion : 62

Re: BONOS GILDEMEISTER

Bono hoy 35,7% valor Par

que dolor !!!

El Lobo de Sanhattan !!

Desconectado

#135 11-12-15 00:42

- Metamorfosis

- Miembro

- Calificacion : 29

Re: BONOS GILDEMEISTER

Desconectado

#136 14-12-15 15:48

- gorgo

- Miembro

- Calificacion : 3

Re: BONOS GILDEMEISTER

Singer es duro.

Desconectado

#137 18-12-15 14:33

- Gabriel_mk2

- Miembro

- Calificacion : 2

Re: BONOS GILDEMEISTER

"In God we trust, Everyone else bring data" - Mike Bloomberg

Desconectado

#138 23-12-15 08:29

- Tatan_79

- Miembro

- Calificacion : 62

Re: BONOS GILDEMEISTER

Y finalmente que paso con este Bono ?

hoy valor Par 34,7 %

y ya se esta hablando de una nueva restructuracion en el 2016-2017

es decir, comprar a 60% valor par era un pesimo negocio.

El Lobo de Sanhattan !!

Desconectado

#139 23-12-15 08:32

- LuckyLeaks

- Miembro

- Calificacion : 102

Re: BONOS GILDEMEISTER

Mucha quita pocas nueces? Bueno ... era riesgosa la cosa, aunque aún está por verse cómo termina.

Desconectado

#140 23-12-15 12:09

- Rolex

- Miembro

Re: BONOS GILDEMEISTER

Volvamos a aquel momento en que supuestamente al controlador lo pusieron de rodillas y le dijeron que le iban a pedir la quiebra...

Bueno otro tema que deja botado USA-CAL, no le apunta, desaparece. SAAM, VAPORES, GILDEMEISTER, y sigue.

Real estate cannot be lost or stolen, nor can it be carried away. Purchased with common sense, paid for in full, and managed with reasonable care, it is about the safest investment in the world

Desconectado

#141 23-12-15 12:13

- Tatan_79

- Miembro

- Calificacion : 62

Re: BONOS GILDEMEISTER

Lo importante es que para gente que esta aprendiendo, nunca sera buen negocio riesgo/retorno comprar a 60% valor par un bono con riesgo claro de default.

Ese tipo de bonos hay que evaluar si es o no negocio a 20%-40% valor par.

El Lobo de Sanhattan !!

Desconectado

#142 23-12-15 14:26

- Gabriel_mk2

- Miembro

- Calificacion : 2

Re: BONOS GILDEMEISTER

Ojalá el usuario USA-CAL, que recomendó comprar los "8,25% Automotores Gildemeister Chile-2021" siga compartiendo su experiencia con nosotros. Al final, todos hemos tenido malas inversiones/transacciones.

En todo caso, al final como toda industria cíclica, en el Largo Plazo se recupera y termina con yield positivo (entre los nuevos bonos y acciones preferentes de nueva emisión).

Sería bueno saber los mark-ups y mark-downs de transacciones apalancadas en bonos corporativos emitidos fuera de Chile y que tal fue su experiencia con las clasificadoras de riesgo que seguían a Gildemeister (PriceWaterhouse, una de ellas).

saludos!!

"In God we trust, Everyone else bring data" - Mike Bloomberg

Desconectado

#143 25-02-16 12:39

- Rolex

- Miembro

Re: BONOS GILDEMEISTER

Automotores Gildemeister Announces Settlement Of Exchange Offer And Consent Solicitation

SANTIAGO, Chile, Feb. 24, 2016 /PRNewswire/ -- Automotores Gildemeister, Sociedad por Acciones (the "Company") announced today the settlement on February 24, 2016 (the "Settlement Date") of the exchange offer and consent solicitation (the "Offers and Solicitation") for its US$400 million 8.250% Senior Unsecured Notes due 2021 (the "Existing 2021 Notes") and its US$300 million 6.750% Senior Unsecured Notes (the "Existing 2023 Notes," and together with the Existing 2021 Notes, the "Existing Unsecured Notes") on the terms previously announced in the offering and solicitation memorandum dated December 17, 2015 (as supplemented from time to time, the "Offering and Solicitation Memorandum"). In connection with the Offers and Solicitation, the Company's Existing Unsecured Notes will be exchanged for 7.50% New Senior Secured Notes due 2021, New Preferred Stock, and Warrants. In addition, pursuant to the Offers and Solicitation, certain amendments to the terms and conditions of the Existing Unsecured Notes were adopted and became effective on the Settlement Date. The New Senior Secured Notes were distributed to participating holders through DTC. The New Preferred Stock and the Warrants were distributed through an international courier service.

In total, 92.2% of the outstanding principal amount of the Existing 2021 Notes and 96.9% of the outstanding principal amount of the Existing 2023 Notes, representing 94.2% of the aggregate outstanding principal amount of the Existing Unsecured Notes, had been validly tendered and accepted Spam the Company for exchange in the Offers and Solicitation. US$31,274,000 in aggregate principal amount of Existing 2021 Notes and US$9,202,000 in aggregate principal amount of Existing 2023 Notes was not tendered and remained outstanding at the Settlement Date.

Participating holders who validly tendered their Existing Unsecured Notes received in exchange for each US$1,000 principal amount of the Existing Unsecured Notes the following consideration:

For the Existing 2021 Notes:

US$645 principal amount of New Senior Secured Notes;

418 shares of New Preferred Stock, divided Spam 1,000; and

One Warrant.

For the Existing 2023 Notes:

US$633 principal amount of New Senior Secured Notes;

410 shares of New Preferred Stock, divided Spam 1,000; and

One Warrant.

In addition, according to the terms of the Offers and Solicitation, because less than 97% of the aggregate outstanding principal amount of the Existing 2021 Notes was tendered, the New Senior Secured Notes will mature on May 23, 2021.This press release is not an offer to sell or a solicitation of an offer to buy any security. The Offers and Solicitation ARE being made solely Spam the OFFERING AND SOLICITATION MEMORANDUM and related letter of transmittal THAT MAY BE OBTAINED FROM THE EXCHANGE AND INFORMATION AGENT and only to such persons and in such jurisdictions as is permitted under applicable law. ANY PUBLIC OFFERING OF SECURITIES TO BE MADE IN THE UNITED STATES WILL BE MADE Spam MEANS OF A PROSPECTUS THAT MAY BE OBTAINED FROM THE COMPANY OR THE SELLING SECURITY HOLDER THAT WILL CONTAIN DETAILED INFORMATION ABOUT THE COMPANY AND MANAGEMENT, AS WELL AS FINANCIAL STATEMENTS.

The New Senior Secured Notes, the New Preferred Stock and the Warrants offered in the Offers and Solicitation will not be registered under the Ley de Mercado de Valores No. 18,045 (the "Securities Market Law"), as amended, of Chile with the Superintendencia de Valores y Seguros (the Chilean Securities and Insurance Commission or "SVS"), and, accordingly, may not be offered or sold to persons in Chile except in circumstances that do not constitute a public offering under Chilean law.

Los valores que se emitan no serán registrados en la Superintendencia de Valores y Seguros de conformidad a la ley de Mercado de Valores No.18,045, por lo que de acuerdo a ello, no podrán ser ofrecidos a personas en Chile excepto en circunstancias que no constituyan una oferta pública de valores de acuerdo a ley Chilena.

About Automotores Gildemeister

Automotores Gildemeister is a vehicle importer and distributor primarily in Chile and Peru. Since 1986, the Company has been the sole distributor of Hyundai passenger and light commercial vehicles in Chile and since 2002, the sole distributor of Hyundai passenger, light commercial and heavy commercial vehicles in Peru.

Exchange and Information Agent

Prime Clerk, LLC

830 Third Avenue, 3rd Floor

New York, NY 10022

c/o Automotores Gildemeister Exchange Offer

Domestic and Canada Toll-Free (844) 205-4334

Outside the US and Canada (917) 606-6438

Email: [email protected]SOURCE Automotores Gildemeister

Y renovo contrato por 2 años mas con hyundai, no es erroneo al final eso de endeudarse con ganas para que los prestamistas pasen a tener un problema con el deudor, y no al reves.

Fijo queda otra pasadita.

Real estate cannot be lost or stolen, nor can it be carried away. Purchased with common sense, paid for in full, and managed with reasonable care, it is about the safest investment in the world

Desconectado

#144 25-02-16 12:59

- USA-CAL

- Miembro

- Calificacion : 80

Re: BONOS GILDEMEISTER

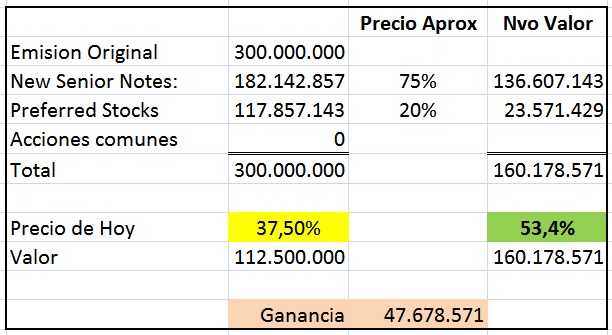

Arriba las matemáticas del anuncio posteado arriba (de fecha de ayer)

Por lo bajo la recuperación será un 53,4% del total emitido. Para respaldar ese calculo, asumo que los nuevos bonos Vcto 2021 se debieran por lo bajo transar a un Tir del 13% pa (75% valor par) las acciones preferentes a entregar les asigno un valor del 20% del valor de caratula y las acciones comunes les asigno un valor CERO.

Definitivamente mi recomendación a todos - cuando esto estaba en 38% - antes del final de la conversión anunciada ayer era una apuesta muy razonable (inviertes 38 y sacas 53; retorno de 39,5% de retorno en menos de 6 meses.... Esto aunque algunos les cueste verlo....

En el mercado de bonos existe la posibilidad de hacer trading con el objetivo de ganar ganancias de capital y no diferenciales de intereses (inversionistas a termino).

RLessman aquí perdió prácticamente todo.... existe la posibilidad aun de tomarse la empresa via la compra de las acciones comunes y sacar a RL...si ello es asi..esas acciones valdrán mas que Cero, posiblemente las acciones preferentes valgan mas 1ue el 20%....y la posibilidad de hacer ganancia para los que inviertan esta abierta.....

Esta apuesta es mejor que comprar una casa en Santiago centro...como prefieren otros.

USA-CAL

“There are two kinds of forecasters: those who don’t know, and those who don’t know they don’t know.” – J.K. Galbraith

Desconectado

#145 25-02-16 13:38

- Rolex

- Miembro

Re: BONOS GILDEMEISTER

en restructuraciones , no hay primera sin segunda.

El bono nuevo que te van a pasar, fijo que te lo reestructuran de nuevo en un año mas, con una nueva "quita"

Y ahora a sentarse a esperar que suceda esto, que va a suceder (siendo generoso) en no mas de 2 años, si al controlador lo tuvieron de rodillas (supuestamente) y termino en que todo fuera un exito, no quiero ni imaginar la proxima quita ![]()

De profesionales aca, te vendo algo en 100, te pago un poco de intereses para que disfrutes, te lo quito y te lo revendo en 60, te pago otro poco de intereses, te lo vuelvo a quitar, ya te pago 10, no te pago ningun interes, sigo funcionando tu pierdes tu inversion, flor de negocio.

El tipo sabe, inversionistas entregados.

Real estate cannot be lost or stolen, nor can it be carried away. Purchased with common sense, paid for in full, and managed with reasonable care, it is about the safest investment in the world

Desconectado

#146 25-02-16 14:03

- Tatan_79

- Miembro

- Calificacion : 62

Re: BONOS GILDEMEISTER

Comprar un bono al 47% valor par

Que defaultee o quiebre la empresa y ganar plata con eso ???Seria un caso único, en promedio el valor de un bono en default no vale mas de un 20% -25% del valor par

Por otra parte por lo general de una empresa en esta situación siempre están inflados los balances en cuanto a activos y patrimonio, por lo que el valor de liquidación es siempre muy menor a lo que dice el balance

hace un año.

y claro cercano al 50% valor par comprar un bono con ese riesgo, NO es negocio.

Al 37%-38% valor par (precio actual), podria ser.. no me gusta para nada, pero es evaluable.

El Lobo de Sanhattan !!

Desconectado

#147 25-02-16 14:43

- USA-CAL

- Miembro

- Calificacion : 80

Re: BONOS GILDEMEISTER

Tata_79...No seas porfiado...o simplemente quieres llevar la contra -como algunos en tema Burbuja inmobiliaria que intentan quedarse siempre con la ultima palabra incluso diciendo.....me lo dijo mi abuelo.....-. Entiendo que un abogado no entienda de finanzas y se peine con las cifras el conservador de bienes raíces....pero este tema es intermediacion de renta fija (bonos high yield) y esta bien que el no entienda...

Hace un ano recomende comprar los bonos a 47% como tu haces referencia.....nunca pensando en guardarlos a termino y sacar 100...... Si tu hubieras comprado a 47, hubieras ganado el cupón de 8,25% lo que sobre tu inversion de 47 te daba un retorno por intereses del 17,55% en el ano.

Adicionalmente, hubieras comprado el bono a 47% y lo podrías vender mañana -luego del ano- en el mercado secundario a un precio de 53,4% lo que te representa una rentabilidad adicional (por ganancia de capital; o diferencia de precio entre venta y compra del bono) de 13,61%

O sea, si hubieras comprado el bono a 47, en 12 meses hubieras ganado un 31% sobre los fondos invertidos en el bono gildemeister....

“There are two kinds of forecasters: those who don’t know, and those who don’t know they don’t know.” – J.K. Galbraith

Desconectado

#148 25-02-16 15:36

- Rolex

- Miembro

Re: BONOS GILDEMEISTER

Tata_79...No seas porfiado...o simplemente quieres llevar la contra -como algunos en tema Burbuja inmobiliaria que intentan quedarse siempre con la ultima palabra incluso diciendo.....me lo dijo mi abuelo.....-.

Don USA-CAL, mantengamos el respeto y paremos con los ataques familiares. Ya segunda vez que se lo pido, si no cuesta nada debatir como la gente, ahora si no le gusta que alguien menor le lleve la contra, digalo al menos y listo, pero con respeto. Le pido comprension, y le aclaro que no soy abogado, y afortunadamente, jamas empleado de nadie.

Sobre GILDEMEISTER, el no querer aceptar que habra otra quita es valido, hasta que sucede y creo que varios aca saben que no hay primera sin segunda, asi funciona.

Real estate cannot be lost or stolen, nor can it be carried away. Purchased with common sense, paid for in full, and managed with reasonable care, it is about the safest investment in the world

Desconectado

#149 29-02-16 14:20

- USA-CAL

- Miembro

- Calificacion : 80

Re: BONOS GILDEMEISTER

Interesante como termina la negociación entre Fondos Buitres y Argentina

Argentina pagará 75% de la deuda....La solución para los inversionistas de renta fija no es nada de mala....sobre todo para aquellos que compraron en mercado secundario los bonos en pasados 4 años a precio 20% del valor par.

Este ejercicio muestra el atractivo de invertir/tradear mercado de Bonos de renta fija de altísimo riesgo.....

El deal no es comprar a 20 para esperar que me paguen 100....es comprar a 20 para vender en mercado secundario a 30...y ganar 50% sobre capital invertido...tradeando el riesgo de crédito del emisor.

USA-CAL

Spam Katia Porzecanski, Charlie Devereux and Bob Van Voris

(Bloomberg) -- Paul Singer versus the republic of Argentina is over.

Some 15 years after the country carried out the biggest sovereign default ever, and 13 years after the hedge-fund billionaire sued for full repayment, the two sides reached a settlement late Sunday. The deal marks a major milestone for Argentina and its new president, Mauricio Macri, restructuring the lions share of the debt remaining from the default and freeing up the nation to tap international markets for much- needed financing as its commodities-based economy falters.

It also brings a close to a bruising, at times ugly, conflict that cost both sides dearly over the years -- in legal fees, lost investment opportunities and countless headaches.

Argentina had even become something of a pariah state, unable to fly its presidential plane or dock its naval ships in some cities abroad out of fear theyd be seized Spam Singers lawyers.

In financial circles, the two names will be forever linked, like George Soros and the Bank of England or Jim Chanos and Enron.

And their drawn-out feud serves as a cautionary tale for both cash-strapped governments flirting with default and the combative speculators looking to fight them in court.

Its definitely the longest, high profile holdout case Ive ever seen, said Edwin Gutierrez, a money manager at Aberdeen Asset Management. There are some, but none have been this high profile and of this magnitude.

Argentina will pay $4.65 billion in cash to Elliott and hedge funds Aurelius Capital Management, Davidson Kempner, and Bracebridge Capital -- which is 75 percent of the principal and interest of their total claims, according to court-appointed mediator Daniel Pollack. The country will also pay some of the holdouts legal fees, as well as a settlement for claims outside of New York. The nation will raise the funds in overseas bond markets to do so, he said.

We are pleased to have reached an agreement with Argentina, Elliott said in a statement. We are hopeful that the completed negotiations, held under the aegis of Special Master Daniel Pollack, have cleared the way for other plaintiffs to reach satisfactory resolutions as well.

Finance Minister Alfonso Prat-Gay and Finance Secretary Luis Caputo will hold a press conference at 6 p.m. in Buenos Aires, according to a ministry official.

After years of dealing with former President Cristina Fernandez de Kirchners intransigence on the issue and seeming disrespect for U.S. law, New York courts have lauded Macris efforts to make good on his campaign pledge to put an end to the litigation shortly after beginning his term in December.

Officials began traveling to New York to meet with creditors in January and published their first proposal to creditors Feb. 5.

Yesterdays agreement is an improvement from the original offer of 72.5 percent of claim, and prior restructurings that imposed losses of about 70 percent on holders of the defaulted bonds. About 7 percent of creditors, including Elliott, rejected those terms and pursued repayment in court.

It was a contentious affair that bordered on the uncivilized on many occasions, like when Fernandez called the 85-year old judge who for years has presided over the case senile or referred to Singer as a Vulture Lord and bloodsucker.

As Singer ramped up his efforts for repayment -- at one point he briefly seized a naval vessel -- the feud evolved beyond an issue of paying ones debts into one of defending national pride and sovereignty Fernandez tried to pass along onto the next generation. Video games, board games and cartoons were created to teach children about the dangers of vulture investors, and the business school at the University of Buenos Aires boasts a debt museum devoted to the saga. After Argentina won the World Cup semifinals in 2014, the crowds patriotic victory chants devolved into a profanity-laced taunt of the hedge funds.

Even toward the end, as Macris team took over the talks with the attitude that combative rhetoric doesnt help, the two sides were still sniping at each other: the hedge funds described Argentinas recent legal tactics as manipulative and abusive, while Prat-Gay has said that if talks stall, its not our fault.

Ultimately, Pollack said of the Argentine officials involved in the talks that their course-correction for Argentina was nothing short of heroic, while Singer was the central figure who involved himself intensely with me over the past several weeks on behalf of the holdout bondholders. He was a tough but fair negotiator.

Argentine bonds rose Monday, with prices on dollar bonds due 2033 jumping to 117.8 cents on the dollar. Yields on current Argentine-law bonds due 2017 declined to 6.41 percent.

The agreement comes weeks after Argentina agreed to pay almost $2 billion to other holdouts, as well as another $1.34 billion to 50,000 Italian bondholders.

The accord with Elliott is subject to approval from the Argentine Congress, which also needs to repeal a law that currently prevents the country from proposing terms to the holdouts that are better than those the nation offered creditors in restructurings. Congress reconvenes in March. Pollack said he hopes the parties will take all necessary steps to complete the settlement in six weeks.

I dont think the terms of this agreement would be the reason why they dont get this approved, said Diego Ferro, co- chief investment officer of Greylock Capital Management.

Theres nothing outrageous or surprising about this deal for the opposition to use it as an excuse."

The agreement marks the resolution of about 85 percent of claims from bondholders with so-called equal treatment injunctions, said Pollack. He will continue to broker negotiations between Argentina and the remaining creditors, he said.

With approval from U.S. District Judge Thomas Griesa, the settlement will probably allow for the release of about $3 billion of interest payments that hes blocked since June 2014 and the reversal of his equal-treatment orders prohibiting Argentina from paying restructured bonds unless the holdouts were also paid. Fernandez had refused to comply with the ruling, pushing the nation into a second default.

After eight years of Fernandez policies that put off investors, Macri needs to lure foreign money to revive a faltering economy and help restore foreign-currency reserves that hit a nine-year low in December. Within his first week in office, he lifted capital controls that had prevented companies from repatriating dividends and devalued the peso, ending years of a crawling peg that kept the currency overvalued as inflation soared.

The accord with the holdouts is the final step to allow Argentina to return to international credit markets. The country, which hasnt sold bonds abroad since the default, has settled arbitration cases at the World Bank, paid Spanish oil company Repsol SA for the expropriation of YPF SA and negotiated with the Paris Club of creditor nations.

Alejo Costa, the head of strategy at Buenos Aires-based brokerage Puente, estimates Argentina will need to issue about

$11 billion dollars to pay the holdouts and an additional

$8 billion dollars to fund fiscal needs.

We believe that amount will put some pressure on yields,

he said. Most of the demand will have to come from investors with a constructive view on Argentina, which will require the government to do a good job communicating its strategy on the fiscal and monetary side

“There are two kinds of forecasters: those who don’t know, and those who don’t know they don’t know.” – J.K. Galbraith

Desconectado

#150 29-02-16 15:15

- Rolex

- Miembro

Re: BONOS GILDEMEISTER

Nadie duda que sea buen negocio, pero los casos son distintos creo yo. Por comparar, gildemeister se parece mas a la araucana que a argentina.

Real estate cannot be lost or stolen, nor can it be carried away. Purchased with common sense, paid for in full, and managed with reasonable care, it is about the safest investment in the world

Desconectado